On April

4, the US Department of Commerce succumbed to protectionist pressures

and chose to launch investigations to check whether textile imports from

China were disrupting US markets. US Commerce Secretary, Carlos Gutierrez,

is reported to have said that the decision was "the first step in

a process to determine whether the US market for these products is being

disrupted and whether China is playing a role in that disruption".

The immediate excuse was evidence of a sharp rise in the quantum of imports

of certain varieties of Chinese textiles into the US market, quota restrictions

on which under the Multi-Fibre Agreement (MFA) were lifted as of January

1, 2005. As Table 1 indicates, import increases during the first quarter

of the year in select categories that are controversial have varied from

an excess of 250 per cent to as much as 1600 per cent. However, there

is need for caution when quoting these figures, because they are growth

rates computed on a base kept low by the MFA's quota regime.

Table 1: Increase in Imports of Specific Categories

of Textiles: Jan-March 2005

|

||||||||||||||||||||

But touting such figures, US industry associations have been accusing the Chinese of dumping to an extent that disrupts the US market and damages the domestic industry. In the event, they are demanding that the government should invoke a clause included in China's WTO accession conditions that permits the US government to restrict import growth to 7.5 per cent a year till 2008. The Bush government that has recently begun its second term has been quick to oblige, even though domestic political pressures are not as overwhelming.

There are, however, a number of reasons to hold that the US response is either alarmist or orchestrated to justify a protectionist response. We must recognise that quotas under the MFA, which limited the quantum of exports into individual segments of the global textile market from the most competitive textile exporters, had two kinds of effects. First, it reduced the competition faced by US (domestic) suppliers of textiles from imports from the most cost-competitive centres of global textile production, allowing the former to sustain higher levels of output. Second, it reduced competition between exporters from more and less competitive locations targeting the same market, by restricting the volume of exports from more competitive producers.

As a result of these two different forces

at play, the lifting of quotas was expected to have two different effects.

One was an increase in the total quantum of imports of restricted items

into individual markets because of increased imports from all locations

that are cost-competitive relative to domestic suppliers. The second was

a re-division of an individual market among exporters, with more cost-competitive

suppliers displacing less cost-competitive ones in individual segments.

|

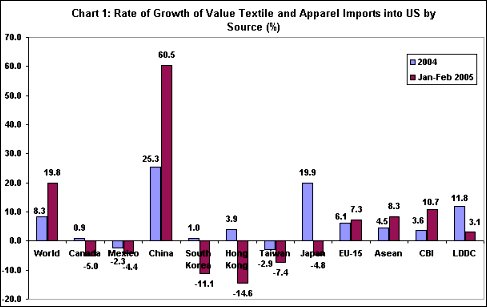

As Chart 1 makes clear, both these tendencies are visible in the US market. Considering all items of textile and apparel imports, the US trade balance report which provides the most comprehensive data, indicates that total imports into the US market rose by close to 20 per cent in the first two months of 2005 (relative to the corresponding period of the previous year) as compared with 8.3 per cent during 2004. Thus the removal of quotas did result in a substantial increase in imports into the US market that would have resulted in some displacement of domestic production.

However, the increase in imports from

China, which amounted to 60.5 per cent during January-February 2005 as

compared with 25.3 per cent in 2004, was not wholly directed at the displacement

of US production. Rather, increased imports from China were accompanied

by a decline or slowing down of imports from other sources such as Mexico,

South Korea, Hong Kong, Taiwan province of China and Japan. That is, after

the removal of quotas, Chinese imports were outcompeting imports into

the US from other sources that were earlier "protected" by the

MFA regime.

|

This is not to say, however, that China is wiping the floor clean. There are other countries such as the EU-15, the ASEAN countries and countries belonging to the Caribbean Basin Initiative (CBI) that have been able to increase the rate of expansion of their exports. What is disconcerting however is that the Least Developed Countries (LDCs), which do not receive the same special benefits as the CBI group in US markets, have seen a significant decline in the rate of growth of their exports to the US market. But this may partly be due to the disruption caused by the tsunami in at least some of these countries, such as Mauritius.

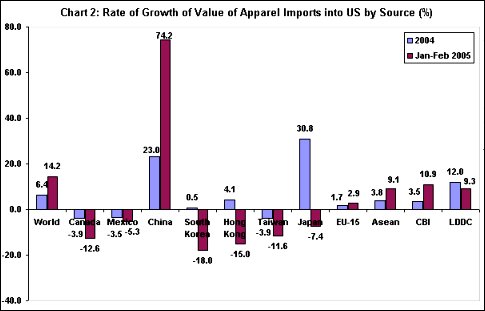

Some of these features are sharper if we consider an area like apparel, which is where the bulk of the increase in imports into the US from China has taken place. As Chart 2 indicates, while China's apparel exports to the US grew by close to 75 per cent during the first two months of 2005, as compared with 23 per cent during 2004, this was accompanied by a substantial degree of displacement of imports from Canada, Mexico, South Korea, Hong Kong and Taiwan province of China. Further, besides increases in imports from country-groupings such as the EU-15, ASEAN and the CBI, LDCs have registered a much smaller decline in the rate of growth of imports than is suggested by aggregate figures.

In sum, not all of China's dramatic export

increase during the first quarter of 2005 was on account of the displacement

of US production. It was partly because of displacement of export increases

from other countries. And there were countries other than China which

contributed to the growth in overall textile imports into the US. Above

all, as Table 2 makes clear, the effect of the increase in Chinese exports

on exports to the US from individual developing countries has not been

as adverse as had been expected.

Table 2: US Textile Imports by Country Major Shipper's

Report ($ Mill.)

Growth Rate |

||||||

2003 |

2004 |

Jan-Feb 2004 |

Jan-Feb 2005 |

Jan-Feb 2004 |

Jan-Feb 2005 |

|

| World | 77434 | 83312 | 12284.1 | 14010 | 7.6 | 14.0 |

| China | 11608.8 | 14559.9 | 2002.9 | 3362.4 | 25.4 | 67.9 |

| Asean | 11678.2 | 12143.6 | 1867.7 | 2014 | 4.0 | 7.8 |

| CAFTA | 9244.6 | 9578.6 | 1266.9 | 1408.4 | 3.6 | 11.2 |

| EU-15 | 4336.5 | 4530 | 687.5 | 730.9 | 4.5 | 6.3 |

| Sub-Sahara | 1534.9 | 1781.8 | 253.2 | 282.5 | 16.1 | 11.6 |

| Bangladesh | 1939.4 | 2065.7 | 324.6 | 359.4 | 6.5 | 10.7 |

| Cambodia | 1251.2 | 1441.7 | 234.3 | 259.1 | 15.2 | 10.6 |

| Fiji | 79.6 | 85.8 | 13.9 | 7.7 | 7.8 | -44.6 |

| India | 3211.5 | 3633.4 | 588.1 | 737 | 13.1 | 25.3 |

| Indonesia | 2375.7 | 2620.2 | 445.4 | 477.6 | 10.3 | 7.2 |

| Japan | 522.4 | 641.7 | 78.3 | 79.8 | 22.8 | 1.9 |

| South Korea | 2567 | 2579.7 | 393.9 | 344.3 | 0.5 | -12.6 |

| Laos | 3.9 | 2.1 | 0.3 | 0.1 | -46.2 | -66.7 |

| Malaysia | 737.5 | 764.3 | 117.3 | 109.8 | 3.6 | -6.4 |

| Maldives | 93.7 | 81 | 12.5 | 4.7 | -13.6 | -62.4 |

| Mauritius | 269.1 | 226.6 | 43.1 | 37.5 | -15.8 | -13.0 |

| Mexico | 7940.8 | 7793.3 | 1144.9 | 1097.2 | -1.9 | -4.2 |

| Mongolia | 181.1 | 229.1 | 25.8 | 21.7 | 26.5 | -15.9 |

| Nepal | 155.3 | 130.6 | 25.9 | 16 | -15.9 | -38.2 |

| Pakistan | 2215.2 | 2546 | 371.4 | 396.9 | 14.9 | 6.9 |

| Philippines | 2040.3 | 1938.1 | 323.6 | 299.9 | -5.0 | -7.3 |

| Singapore | 270.8 | 244.1 | 34.1 | 34.1 | -9.9 | 0.0 |

| Sri Lanka | 1493 | 1585.2 | 258.6 | 305.5 | 6.2 | 18.1 |

| Taiwan Province of China | 2185 | 2103.9 | 308.3 | 283.6 | -3.7 | -8.0 |

| Thailand | 2071.7 | 2198.2 | 314.1 | 372.8 | 6.1 | 18.7 |

| Vietnam | 2484.3 | 2719.7 | 361.8 | 430.2 | 9.5 | 18.9 |

What needs to be noted is that the displacement of US production, to the extent that it occurred, is a sign that the US has not adequately restructured its industry during the long years of protection resorted to for this very purpose. The protection afforded to developed country textile production with the aim of restructuring those industries began in the 1961, when the Long Term Agreement on textiles was signed. That agreement provided the developed countries with a 10-year respite, during which they were expected to either phase out a part of their uncompetitive textile production, "burdened" by high wages, or modernise their textile industries to render them competitive.

The promise to do away with protection in ten years did not materialise. Protection was continued under the Multi-Fibre Agreement, which was once more scrutinised for phase-out under the Uruguay Round Agreement of 1994. But even under that agreement, the phase-out of quotas was back-loaded, with quotas on close to half of global textile trade kept in place till January 1, 2005. It is well known that most developed countries first lifted quotas on items of less relevance to developing country trade, reserving true liberalisation till the beginning of 2005.

What the first-quarter surge in textile exports to the US indicates is that despite 45 years of protection expressly justified by the need to restructure the industry, the US has not done so, unlike countries such as the UK whose dependence on textiles during the early stages of their industrialisation was even greater. But the US is not the only culprit. Even countries in the EU (such as France and Italy) are using the US resistance to the Chinese export surge as the basis for a demand for greater protection for their own textile production. The European Union's trade commissioner, Peter Mandelson, has been resisting pressure to impose restrictions on Chinese textile imports, on the grounds that the available evidence of market disruption is inconclusive and could not justify curbs for the time being. However, his ambivalent postures, resulting from differences within the Community, suggest that the EU too might resort to import curbs. Responding to calls from countries like Sweden not to impose such curbs, since that would amount to protectionism, Mandelson declared: "We should not confuse protection with protectionism."

All this controversy arises despite efforts by China to dampen the growth of its textile exports since January 2005 to temper the reaction to likely export increases. In December 2004, China imposed export tariffs of Rmb0.2-Rmb0.3 per item in some cases and Rmb0.5 per kilogramme in others in response to concerns in the US and Europe that Chinese textile exports might surge following the expiry of quotas on January 1. Now, China is contemplating further export tariffs. Expectations are that China might raise export tariffs by as much as Rmb2-Rmb4 per piece. Such action is being contemplated despite the danger that Chinese exporters are likely to be badly hit, because prices for garment orders are fixed several months before shipment.

China's need to bend over backwards to placate the US results from three factors. First, China's own dependence on the US market for exports that have become a major engine for its growth. Second, the huge trade and current account deficit on the US balance of payments, which is resulting in a depreciation of the dollar and rising the spectre of a financial crash and global recession. Third, the huge US trade deficit with China that the former wants to reduce by getting China to revalue its currency. The message is clear, if developing countries record a deficit on their balance of payments it is their problem and a reflection of their mismanagement. If the US records a deficit on it external account that is everybody's problem and a reflection of a global "imbalance" that needs correction.

Unfortunately, imposing curbs on Chinese

textile imports into the US or the EU may not resolve the problem either

of unemployment in the US and EU textile industries or the deficit on

the US trade account. It would merely serve to increase textile exports

from other developing countries to the US and EU. But the fact that this

could be used to divide developing country exporters and win the support

from some of them in the battle against China may suit the US and EU.

It helps win allies in the battle to force China to turn inwards rather

than grow on the basis of burgeoning exports. Globalisation is good only

when the USand perhaps the EU reaps its benefita. If that does not happen,

protectionism or voluntary export restraint is the preferred alternative.