The dollar is on the decline, with its

value having fallen by around 30 per cent relative to other major currencies

since 2002 and by close to 20 per cent in trade-weighted terms. Yet, the

US government feigns being unconcerned with the problem. In the G-20 meeting

held in the second half of November, the US Treasury Secretary reportedly

refused to talk about the dollar's decline, though he reiterated the Bush

administration's public commitment to halve the US government's budget

deficit during its second term and bring it below two per cent of GDP.

The relevance of the budget deficit for the problem at hand is obvious,

given the connection between the dollar's decline and the twin deficits

in the USthe balance of payments deficit amounting to 5.5 per cent of

GDP and the fiscal deficit to 4.2 per cent of GDP. With savings rates

close to zero on average, private spending is high in the US. But a large

part of the demand this generates spills over into the international market

given the lack of competitiveness of US producers. However, this has not

resulted in a domestic recession because the government has in recent

years been pump-priming the economy with deficit spending (though a part

of that too leaks out abroad). In the event, the US has required the two

deficits to sustain its reasonable rate of growth by developed country

standards.

These deficits have not proved a problem because of capital inflows, including

in the form of investment of surpluses accumulated by foreign governments

and central banks in dollar denominated financial assets. According to

one source, in 2002, 2003 and the first half of 2004, foreign governments

financed $564bn (43 per cent) of a cumulative current account deficit

of $1,318bn (£695bn). The problem recently has been that both private

wealthholders and foreign governments have begun to fear that the unsustainable

value of the dollar spells a decline in the currency that could sharply

erode the value of their assets. The resulting rearrangement of their

portfolio away from dollar assets in favour of other currencies is what

explains the dollar's decline.

At one level this decline appears to be a boon to the US. It cheapens

the foreign exchange value of its exports and renders imports more expensive

in dollar terms, improving US competitiveness. If this helps reduce the

trade deficit, the size of the fiscal deficit needed to keep growth going

would be lower. A process of self-correction seems to be providing a solution

to the twin deficit problem.

The difficulty, however, is that the dollar's decline would also result

in lower inflows into and larger outflows into US capital markets, resulting

in a fall in financial asset prices that would reduce the wealth position

of US households and institutions. This would reduce consumer spending

and curtail demand. That problem could be aggravated by a possible liquidity

crunch in the system, as banks and financial institutions experiencing

a depreciation of their asset values turn cautious. Further, lower financial

asset prices imply higher interest rates that could affect investment

adversely as well. Thus a correction of the twin deficit problem through

a depreciation of the dollar could also imply a recession in the US.

All this makes the dollar's decline a problem for the rest of the world

as well, especially countries in Europe and in Asia, like China, that

are heavily dependent on the US market. Dollar depreciation increases

the dollar value of their exports to the US and undermines their competitiveness

and recessionary trends in the US would squeeze an important market for

their exports.

It is this global effect of the dollar's decline that the US exploits

to make the decline everybody's problem and not just its own. In its view,

the twin deficit problem can be best resolved through increased net exports

(exports net of imports) from the US. This would reduce the trade deficit,

contribute to demand for US goods and help reduce the fiscal deficit without

affecting growth adversely. So, Europe, Japan and China must help raise

net exports from the US.

The G-20 meeting in November saw the Europe and Japan partly going along

with the US on this count. ''The Group of 20 leading rich and emerging

market nations have agreed on a co-ordinated effort to reduce global trade

imbalances by cutting the US fiscal deficit, reforms to boost growth in

Europe and Japan and increasing exchange rate flexibility in Asia,'' reported

the Financial Times on November 22. That is, the reduction of the US fiscal

deficit was made contingent on reflation in Europe and Japan which, hopefully,

would expand the market for US goods, and reduced currency intervention

by Asian governments aimed at pegging their currencies to the dollar.

The latter, by resulting in an appreciation of Asian currencies vis-à-vis

the dollar is expected to increase the competitiveness of US exports to

these countries and therefore in an increase in the volume of US exports.

The country which would be most effected by the second of these recommendations

is China, which has pegged the value of its currency the renminbi (yuan)

at 8.27 to a dollar since 1997. China has been under pressure for quite

some time to revalue its currency and redress the ''imbalance'' that its

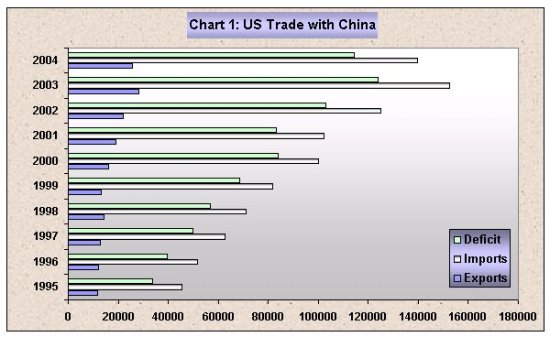

trade surplus ($124 billion last year) with the US (Chart 1) and its large

foreign exchange reserves ($514.5 billion) ostensibly reflect. That pressure

has now increased, since Europe and Japan would like to see China bearing

a larger share of the burden of global adjustment, by curtailing its exports

and increasing its imports with a flexible and appreciating currency.

China's fears on this count are not just related to its trading position.

It is more worried about the effects of introducing a more flexible currency

and allowing the yuan to appreciate on its currency and financial markets.

A stronger yuan is bound to spur large capital inflows, while capital

account restrictions do not permit money to flow out easily. This would

increase reserves further and drive the yuan even higher. And once that

happens, speculation on the value of the yuan can increase capital inflows

even more. Such a spiral can be destabilising and weaken autonomy in monetary

policy.

Not surprisingly, China is not happy. In an interview with the Financial

Times, Li Ruogu, the deputy governor of the People's Bank of China, warned

the US not to blame other countries for its economic difficulties. ''China's

custom is that we never blame others for our own problem,'' he reportedly

said. ''For the past 26 years, we never put pressure or problems on to

the world. The US has the reverse attitude, whenever they have a problem,

they blame others.''

There were three unexceptional arguments that Li used to justify his criticism.

First, "The savings rate in China is more than 40 per cent. In the

US it is less than 2 per cent. So the problem is that they spend too much

and save too little." Second, there was a lack of correspondence

between US wages and productivity resulting from the tendency of the government

to protect low productivity jobs. US workers enjoyed relatively high wages

but remained excessively engaged in low value-added industries such as

textiles and agriculture. Finally, US policies discriminate against exports

of goods that China needs. Restrictions on exports of military and high-technology

products to China partly explains Beijing's huge trade surplus with America,

he argues.

In fact, the evidence on China's trade does not support the view that

it adopts a mercantilist policy that pushes exports and restricts imports.

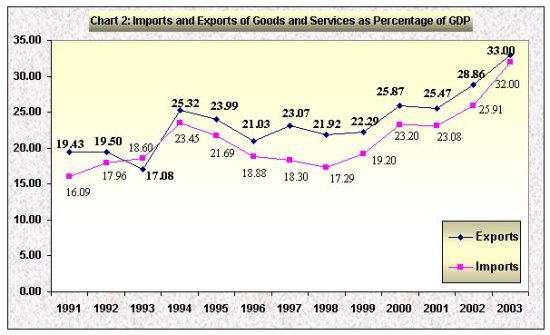

In 2003, while exports of goods and services amounted to 33 per cent of

GDP, imports of goods and services stood at 32 per cent of GDP (Chart

2). At present, China records an overall trade deficit, which is expected

to touch $40 billion in 2004. In the first four months of 2004, China's

exports amounted to $162.7 billion, up 33.5 per cent from a year ago.

Imports on the other hand rose 42.4 per cent to $173.5 billion, resulting

in an overall trade deficit of $10.8 billion. A negative trade balance

is sure proof that mercantilism does not drive trade and economic policy.

The reason why China is susceptible to international pressure despite

this trade record is the country-wise distribution of its exports and

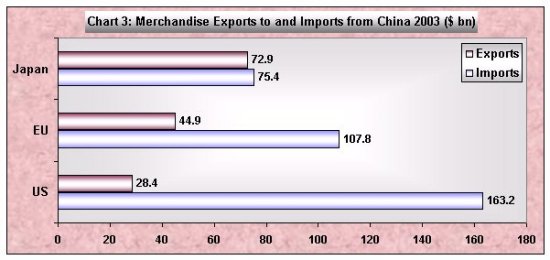

imports. In 2003, merchandise imports from China into the US amounted

to $163.2 billion, or 12.5 per cent of its total merchandise imports.

This figure had risen from 6.3 per cent in 1995. Imports into the European

Union and Japan amounted to $107.8 billion (3.7 per cent) and $75.4 billion

(19.7 per cent). Though relative to the total Japan was a major importer,

the US clearly dominated in absolute magnitude. What is more, merchandise

exports to China in 2003 stood at $28.4 billion, $44.9 billion and $72.5

billion respectively in the case of the US, European Union and Japan.

The US sucks in commodities from China, but sends little back in return.

Finally, in recent years, China has provided space for foreign firms in its domestic market. As Nicholas Lardy, then of the Brookings Institution, wrote in 2002: At the turn of the twenty-first century in China, ''foreign manufacturers led by Motorola, Nokia and Ericsson had captured 95 per cent of the market for cellular phones. Coca-Cola was the dominant supplier of carbonated beverages with a market share fifteen times its closest domestic competitor. Its operations in China have been profitable for more than a decade, and Coca-Cola expects China to emerge as its largest Asian market in 2002 or 2003. McDonald's and Kentucky Fried Chicken, with almost 900 outlets between them, dominated China's rapidly growing food market. Kodak had captured half the market for film and photographic paper. Volkswagen, through two separate joint ventures, controlled more than half the domestic automobile industry. Carrefour, the French company, had become China's second largest retailer only five years after entering the market. And, as unlikely as it might have once seemed, Proctor and Gamble had more than half of what is undoubtedly the world's biggest shampoo market.''

Thus, the problem is not one of Chinese mercantilism, but one of lack

of competitiveness of the US. Not surprisingly, the US has performed poorly

despite the fact that the yuan is pegged to the dollar. With the dollar

depreciating vis-à-vis the euro and the yen, it is the EU and Japan

that should lose out in trade with China, not the US.

Despite all this evidence in its favour, China is feeling the heat, as

shown by Li Ruogu's response. This is the result of China's reform-driven

dependence on exports in general and exports to the US in particular.

With exports amounting to 33 per cent of GDP and the US accounting for

37 per cent of China's total merchandise exports of $438.4 billion, the

US market is too important for China for US views to be ignored. Not surprisingly,

expectations are that China would soon loosen strings on the yuan, which

has since 1995 been allowed to fluctuate only within a ultra-narrow 0.3

per cent band around 8.28 yuan to the dollar. That band is now expected

to widen. But this is likely to be too slow to satisfy the US because

of what investment banker Henry Liu sees as China's ''residual commitment

to socialist principles'', which makes it hope that it can ''reap the

euphoria of market fundamentalism without succumbing to its narcotic addiction.''

The US and the rest of the world will have to find some other answer to

the problem of the weakening dollar generated by the twin deficits in

the US.