It is a truism that economic reform in

China has meant a substantial expansion in the role of private initiative

in economic activity. The dismantling of communes and collectives, the

encouragement of foreign investment, the recognition of the private sector

initially as a "supplement to the state-owned economy" and subsequently

as an "important component of the socialist market economy",

the closure, restructuring and disinvestment of shares of enterprises

in the state-owned sector, the opening of Communist Party of China (CPC)

membership to entrepreneurs and businesspersons, the sale of equity in

leading state-owned banks and most recently the decision to make all state-held

shares in the1,300 listed companies publicly traded, have all contributed

to a substantial expansion in the role of the private sector, and continue

to do so.

As this process has been unfolding, Western observers have repeatedly

sought to assess the relative roles of the private and state sector in

the Chinese economy. The reasons for this interest are not difficult to

identify. To start with, it could be argued that as and when the private

sector overtakes the public sector in China's economy, the only example

of a large economy with substantial state ownership and control vanishes,

leaving no living example of an significant alternative to predominately

market-driven capitalist economies. But more importantly, many observers

feel that if the private sector displaces the state-sector as the dominant

player in the economy, it would not be long before the CPC would have

to relax its legally unopposed dominance and control over the political,

social and cultural life of the nation. Some have even argued that political

democracy would be an inevitable fall out of a growing role for the market

and the private sector, resulting in a gradual decline in the ideological

sway of the CPC. In sum, China is in their view on the brink of a "velvet

revolution" precipitated by the very state and party that would be

ousted by such a revolution.

This renders significant the release in September of a first survey of

China by the OECD as part of its Economic Surveys series, which is unconventional

since China is not an OECD member. The survey argues that as far back

as 1998 the private sector's share of value added exceeded 50 per cent

both at an economy-wide level and within the business sector. And more

recently in 2001, the report says, the private share of value added crossed

the half way mark in the non-farm business sector as well. The long delay

in recognising that the so-called "transition" had been completed

is attributed to the fact that Chinese Law, which specifies what is an

enterprise and which enterprises can be deemed to be private, and, therefore,

Chinese statistics, make the segregation of the private-controlled component

in different sectors extremely difficult, if not virtually impossible.

Add to this the peculiarities of the transition in China where state-owned

firms, collective enterprises and town and village enterprises are being

gradually corporatised with both other state organisations and private

individuals and institutions acquiring a stake, and the difficulty of

deciding which is private and which is not, only increases.

Thus, Chinese law does not consider a unit with a single industrial or

commercial proprietor employing eight or less workers as an enterprise,

and leaves such units out of the category of private enterprises. Units

deemed to be privately owned enterprises are one of eight categories of

domestically funded enterprises along with state-owned enterprises, collectively-owned

enterprises, cooperative enterprises, joint-ownership enterprises, limited

liability enterprises, shareholding enterprises, and other enterprises.

Besides these there are foreign funded enterprises, including those funded

from Hong Kong, Macau and Taiwan Province of China. Reform has meant that in almost all

these categories, private stakeholders have been accommodated to differing

degrees. But none of them can be considered as being fully private, inasmuch

as some of these enterprises still only have a minority private stake.

Even foreign funded enterprises need not be privately controlled, since

foreign-funded shareholding corporations require only a minimum 25 per

cent foreign capital contribution to registered capital.

The OECD survey attempts to unbundle the data by dropping the official

definition of what is private and using microdata from the National Bureau

of Statistics to arrive at an assessment of the relative size of the private

sector. The survey claims to use a strict definition of the private sector

by separating firms according to type of controlling shareholder: whether

it is the state (directly or indirectly), a collective (local government),

or a private entity (individuals, domestic legal persons, or foreign companies)

that controls the firm. The estimates are made for the business sector

as a whole (including all economic sectors up to distribution and commercial

services but excluding government and non-profit services), which accounted

for 94 per cent of GDP in 1998, as well as for specific components of

that sector such as its non-farm component which accounted for 76 per

cent of GDP in that year. To simplify matters, economic activities included

in GDP that take place outside the official reporting system are assumed

to be in the private sector.

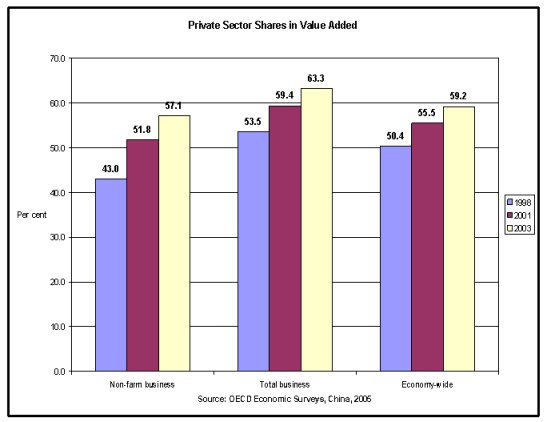

On the basis of this analysis, the survey declares that the Chinese economy

has been characterised by more private than public ownership for some

time now. Thus, the private sector, which accounted for 43 per cent of

value added in the non-farm business sector, was responsible for 57.1

per cent in 2003. The corresponding figures for the business sector and

the economy as a whole were 53.5 and 63.3 and 50.4 and 59.2 respectively.

This is indeed a remarkable transition

What is more, if the analysis is restricted to companies that regularly

produce statistical reports (those with annual sales of over CNY 5 million),

then the private sector's share of valued added has risen from 28 to 52

per cent between 1998 and 2003. Further, in 1998, the private sector contributed

a larger share of value added in only 5 out of 23 "non-core"

manufacturing industries. By 2003 this had risen to cover all 23 of these

industries. In half of those industries, private firms produced more than

three-quarters of output. Overall in these 23 industries, the private

sector is estimated to employ two-thirds of the labour-force, contribute

two-thirds of valued added in these industries, and is responsible for

over 90 per cent of their exports. To top it all, over a quarter of all

industrial output is now reportedly produced by private foreign-owned

companies.

This rapid rise of the private sector implies that it is not just the

result of private firms accounting for a disproportionate share of the

increase in domestic and export markets. The private sector is displacing

the collective state-owned sectors in pre-existing markets as well, partly

as a result of the conversion of these units into private-controlled entities

and partly as a result of their closure. According to the OECD's figures,

about one-third of the increase in the private sector share is mirrored

in a decline in the number and output of collectives, with the remaining

two-thirds reflected in closure and divestment of solely state-owned firms.

It must be noted that, outside the non-farm business sector, to treat

these figures as indicative of the role of private ownership is indeed

an exaggeration. This is because land is by no means privately owned in

much of rural China. Rural land in China is still owned by the village

collective, which allocates land to households predominantly based on

size. Further, even though laws have been passed to provide peasants rights

to a 30-year lease, this has not been implemented in most parts of the

country. The OECD survey itself reports that in 1999, almost two-thirds

of farmers in a random sample of 11 provinces lived in villages that had

not implemented the 30-year lease system. And whatever be the duration

of lease adopted, there are indications that most leases do not foreclose

adjustments of allotments during the lease period. That is while there

is a strong relationship now between household effort and returns earned,

Chinese agriculture cannot be seen as characterised by private ownership

in the conventional sense.

However, this does not undermine the significance of the large and rising

share of private business in the value-added by the non-farm business

sector. But here too the evidence underestimates the role of the state.

To start with private presence in industry is regionally concentrated.

An overwhelming share of private industrial output is produced in the

eastern coastal region (especially Zhejiang, Guangdong and Jiangsu provinces).

In this region, the share of industrial value added attributable to the

private sector is as high as 63 per cent, as compared with only 32 per

cent in other regions. Thus there is a considerable lag in the development

of the private sector in central, western, and north-eastern regions when

compared with the export-oriented eastern coastal region. That implies

the continued persistence of the non-private or state sector. But there

are signs of a faster growth in private activity in the interior regions

as well.

But this is not the only reason why the state remains important. To start

with, the public sector dominates core or strategic areas identified as

the lifelines of the economy, energy the energy, metals, automobile, and

defence industries. Between three-fourths and 95 per cent of value added

in the gas, petroleum, coal mining, electricity and water supply industries

is contributed by the state-owned sector.

Further, the state share in aggregate fixed capital formation remains

high, making it the prime driver of growth. Of the total investment in

fixed assets of CNY 5.6 trillion in 2003, 53 per cent was accounted for

by state-owned units and collectives, and the rest was undertaken in the

"individuals' economy" or by units characterised by other types

of ownership. But since the role of provincial and local bodies in the

other types of units can be substantial, the actual role of the state

in financing fixed investment and growth is still crucial.

But these features of state presence are visible in some market economies

as well, making the characterisation of the Chinese economy and society

a knotty issue. What is clear, however, is that the transition that has

occurred does not seem to have challenged the supremacy of the CPC and

the Chinese government in any way – as yet.

| |